All Categories

Featured

Table of Contents

For the majority of people, the greatest issue with the limitless financial concept is that first hit to early liquidity brought on by the costs. This disadvantage of unlimited banking can be reduced significantly with correct plan layout, the first years will certainly constantly be the worst years with any type of Whole Life policy.

That stated, there are specific unlimited financial life insurance policy plans created mainly for high early cash money worth (HECV) of over 90% in the initial year. The long-lasting efficiency will often significantly lag the best-performing Infinite Financial life insurance plans. Having accessibility to that additional 4 figures in the very first couple of years may come at the expense of 6-figures in the future.

You actually obtain some substantial lasting advantages that aid you recoup these very early expenses and after that some. We locate that this impeded early liquidity trouble with unlimited financial is much more mental than anything else when thoroughly explored. If they definitely needed every penny of the money missing out on from their boundless banking life insurance plan in the initial few years.

Tag: unlimited banking principle In this episode, I speak about finances with Mary Jo Irmen who educates the Infinite Banking Idea. With the rise of TikTok as an information-sharing system, monetary advice and approaches have discovered a novel means of spreading. One such strategy that has been making the rounds is the limitless financial idea, or IBC for brief, amassing endorsements from celebrities like rap artist Waka Flocka Flame.

Within these plans, the cash money worth expands based on a rate set by the insurance company. As soon as a considerable cash worth gathers, policyholders can obtain a cash worth lending. These financings vary from traditional ones, with life insurance acting as security, indicating one could lose their protection if loaning exceedingly without appropriate money worth to support the insurance coverage prices.

And while the appeal of these policies appears, there are innate constraints and risks, necessitating thorough money worth tracking. The method's authenticity isn't black and white. For high-net-worth people or company owner, specifically those using methods like company-owned life insurance coverage (COLI), the advantages of tax obligation breaks and compound growth might be appealing.

Banker Life Quotes

The attraction of infinite banking does not negate its obstacles: Price: The fundamental need, an irreversible life insurance policy plan, is costlier than its term equivalents. Eligibility: Not every person gets entire life insurance coverage due to rigorous underwriting processes that can leave out those with certain health and wellness or lifestyle conditions. Intricacy and risk: The intricate nature of IBC, paired with its risks, might deter numerous, specifically when easier and less high-risk options are offered.

Allocating around 10% of your month-to-month income to the policy is simply not practical for many individuals. Part of what you read below is simply a reiteration of what has currently been stated over.

Before you get on your own right into a situation you're not prepared for, understand the adhering to first: Although the idea is commonly marketed as such, you're not actually taking a funding from on your own. If that were the case, you would not need to repay it. Instead, you're borrowing from the insurance provider and need to repay it with rate of interest.

Some social media articles advise using money worth from whole life insurance policy to pay for bank card financial obligation. The idea is that when you pay off the financing with rate of interest, the quantity will be returned to your financial investments. However, that's not just how it functions. When you repay the funding, a portion of that rate of interest mosts likely to the insurance provider.

For the very first numerous years, you'll be paying off the payment. This makes it extremely difficult for your policy to gather value throughout this time. Unless you can manage to pay a few to several hundred dollars for the following years or even more, IBC won't work for you.

How Can You Be Your Own Bank

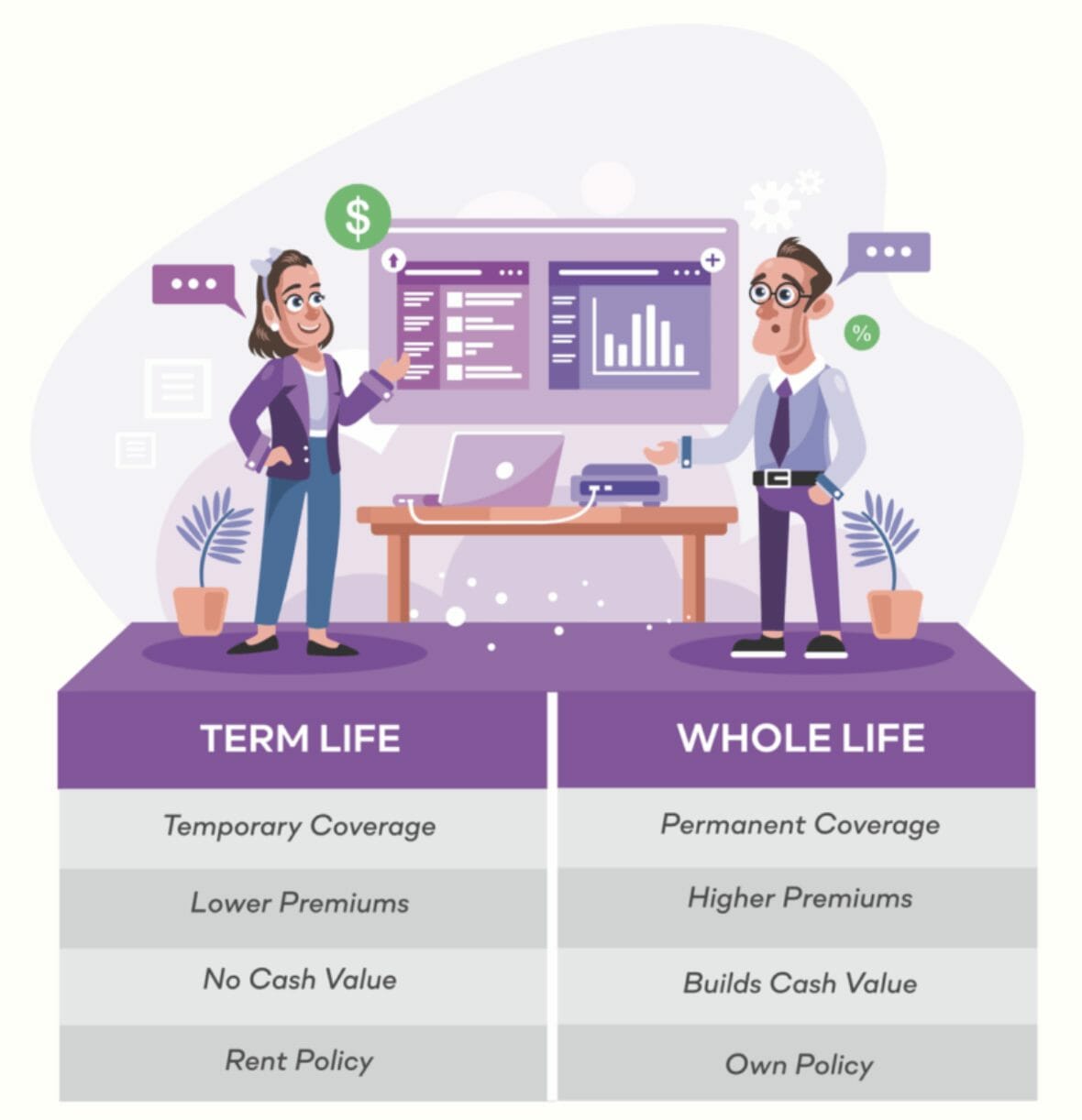

If you need life insurance, below are some beneficial tips to consider: Take into consideration term life insurance. Make certain to go shopping about for the ideal price.

Copyright (c) 2023, Intercom, Inc. () with Reserved Font Name "Montserrat". Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Reserved Font Call "Montserrat".

Td Bank Visa Infinite Card

As a CPA specializing in realty investing, I've cleaned shoulders with the "Infinite Financial Idea" (IBC) a lot more times than I can count. I've also interviewed specialists on the subject. The major draw, aside from the apparent life insurance policy benefits, was constantly the idea of building up cash value within a permanent life insurance policy policy and loaning versus it.

Sure, that makes good sense. Yet honestly, I constantly assumed that cash would certainly be better spent directly on investments instead of funneling it via a life insurance coverage plan Until I uncovered how IBC could be integrated with an Irrevocable Life Insurance Policy Trust Fund (ILIT) to produce generational riches. Let's start with the fundamentals.

Privatized Banking Concept

When you obtain versus your plan's money value, there's no collection repayment schedule, providing you the flexibility to manage the lending on your terms. At the same time, the cash money worth remains to expand based on the policy's assurances and rewards. This arrangement enables you to accessibility liquidity without disrupting the long-term growth of your plan, supplied that the financing and interest are taken care of carefully.

As grandchildren are birthed and grow up, the ILIT can purchase life insurance coverage plans on their lives. Household participants can take finances from the ILIT, making use of the cash money worth of the policies to fund investments, start organizations, or cover major expenditures.

A crucial element of handling this Household Bank is making use of the HEMS standard, which represents "Wellness, Education, Upkeep, or Support." This guideline is often consisted of in depend on arrangements to direct the trustee on exactly how they can disperse funds to beneficiaries. By adhering to the HEMS standard, the depend on makes sure that circulations are made for necessary needs and lasting assistance, securing the trust fund's possessions while still providing for member of the family.

Boosted Versatility: Unlike inflexible small business loan, you manage the settlement terms when obtaining from your own plan. This permits you to framework payments in a manner that aligns with your business capital. infinite banking course. Better Money Flow: By financing overhead via policy financings, you can potentially liberate money that would or else be linked up in typical financing repayments or equipment leases

He has the very same devices, but has actually additionally developed additional cash money value in his plan and got tax benefits. Plus, he currently has $50,000 offered in his plan to use for future possibilities or costs. Despite its possible benefits, some individuals stay doubtful of the Infinite Banking Concept. Let's resolve a few typical problems: "Isn't this just pricey life insurance policy?" While it holds true that the premiums for a correctly structured entire life policy may be greater than term insurance, it is essential to view it as more than simply life insurance coverage.

Private Family Banking Life Insurance

It has to do with producing a flexible funding system that provides you control and supplies several advantages. When made use of purposefully, it can complement other investments and business approaches. If you're fascinated by the possibility of the Infinite Financial Principle for your service, here are some actions to take into consideration: Enlighten Yourself: Dive deeper into the idea via trustworthy publications, seminars, or assessments with well-informed specialists.

{kind=link}

Latest Posts

Infinite Banking Course

Infinite Banking With Whole Life Insurance

How To Become Your Own Bank With Life Insurance